Bidenomics: the Democratic Transition

- Mathias Talmant

- 25 janv. 2021

- 6 min de lecture

The first 100 days

The tradition initiated by Franklin Roosevelt in 1933 determined the “first 100 days” in the office as the most crucial ones for an American President. Joe Biden promised to deliver 100mn vaccines to 100mn Americans in his first 100 days. This goal seems to be farfetched knowing that as of January 24, the federal Centers for Disease Control and Prevention reported that only 5.6% of the total US population or about 20mn people had already received at least one dose of a Covid-19 vaccine, and that about 3.2 mn people had been fully vaccinated.

Source: The New York Times.

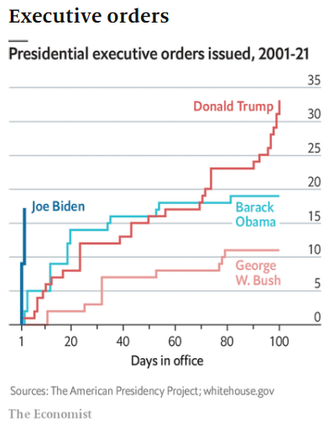

Ready, steady, Joe!

Joe Biden is a centrist who values proletarians more than their antagonists. During his 36 years in Senate, his main passions were the justice system and foreign policy. Notwithstanding age-related jokes, credit where credit is due, Mr Biden has matched words with action by signing a slew of executive orders in his first few days in the Oval Office. Most of them were aimed at stopping the spread of COVID-19. The new Democrat President will not run short of problems as he will have to heal the wounds inflicted by Donald Trump for four years. Two weeks after the raid on the Capitol, Mr Biden called for a moment of national healing. “Without unity, there is no peace, only bitterness and fury.” He must tackle a quadruple crisis: health, economy, environment and homeland security. The fresher the mandate the easier it will be for President Biden to enact legislation because he has not disappointed anyone yet. He still as all the cards in hand to reboot the economy having both the support from chambers of Congress and a high approval rating.

Empirical study of political influence on US economy

Advantage donkeys - statistics are on Mr Biden’s side. According to a study from the National Bureau of Economic Research, based on a 64-year dataset (1947 to 2013), real GDP growth rates under Democratic and Republican presidents were starkly different: 4.35% and 2.54% respectively. In other words, the US economy typically grew by 18.6% over a mandate when the President was a Democrat, but only by 10.6% when he was a Republican. Since the Depression was an outlier to this dataset, if we remove both Roosevelt's and Hoover's results, Democrats gained 3.6% on average while Republicans gained 2.8%. And the variances of quarterly growth rates are roughly equal, so Democratic Presidents preside over growth that is faster, but not more volatile.

Source: Blinder, A. S., Watson M. W. (2014), Presidents and the U.S. Economy: An Econometric Exploration, National Bureau of Economic Research.

As a matter of comparison, according to the same paper, this relationship is reversed in France as right parties generated a 3.42% average yearly GDP growth rate vs 3.19% for left parties, between 1949 and 2012. In addition, average yearly stock returns on the S&P500 were also significantly higher under Democratic administration compared to Republican ones: 8.08% and 2.07% respectively (83% confidence interval).

Donkeys fighting elephants

Empirical data seem to demonstrate that Democrats are better at generating economic growth, but why is this so? One possible explanation is the fact that Democrats have dealt with less recessions than Republicans in the past. However, to answer this question, we need a clearer view of the dichotomy between blue and red philosophies.

On the one hand, Democrats stress out the importance to sustain demand from low-income and middle-income families because they have the largest propensity to consume. They advocate that reducing inequalities fosters economic activity because low-income families are more likely to spend any extra money on necessities instead of saving or investing it. Democrats believe in Keyne’s multiplier effect and government interventionism, which implies that the government should spend its way out of a recession.

On the other hand, Republicans back the supply-side of the economy and typically aim to benefit businesses and investors. Their plan consists in slashing tax on businesses so as to boost employment, in turn increasing demand and growth. In theory, the increased revenue from a stronger economy shall offset the initial revenue loss over time. They promote self-discipline and believe in prosperity without government interference.

Republicans' business-friendly approach leads most people to believe that they are better for the economy, but as we saw previously, data refute this perception. Republicans advocate fiscal responsibility, but they are almost as guilty as Democrats in increasing the debt with short-sighted tax cuts. On the unemployment side, there is no statistical evidence of tax cuts superiority over fiscal spendings. What we can be sure for now is that cabinet-level demographics suggest a more experienced and more diverse team at the helm of the state. However, the future is not bounded by past experiences and Biden may well drift from his peers' track record in this unprecedented economic context.

The Keynesian revival

First of all, President Biden needs to clean the house and undo much of the damage of the Trump era, namely harsh immigration policies, weak environmental protections and poor management of the sanitary crisis. Rejoining the World Health Organisation and the Paris Climate Agreement are already out of the way. Mr Biden’s next order of business will be another COVID-19 relief bill, costing $1.9tn (Republicans may balk at the cost):

$160bn for a national vaccine programme, expanded testing and contact-tracers;

$1,400 stimulus cheque;

Increases in unemployment benefits;

Temporarily enhanced child tax credit.

Soon enough he will implement his most populist ideas. Although he rejected his bluest partisans’ proposals including Medicare for All, the Green New Deal and defunding the police, he retains measures such as minimum-wage increases, industrial policy and substantial government spending. After its “rescue” plan will come a “recovery” bill. The President’s Keynesian philosophy will be cristalised in a massive infrastructure spending, perhaps the $2tn pledged in the campaign. It would also lay ground for Mr Biden’s climate-change pledges. He promised to ensure universal broadband access, spend $400bn on energy and climate research and create 10mn new clean-energy jobs on the way to decarbonising the electricity sector by 2035 and the economy as a whole by 2050.

Deep spendings & shallow pockets

I think Biden's election and Democratic policies are a positive news for the long-term, but they may be a drag in the short-term as public debt builds up to unsustsainable levels. The Congressional Budget Office forecasts federal debt in 2050 twice as high as they were after WWII. As alarming as these figures might look, financial markets turn their eyes away and normal laws of economics are out of touch with reality. Interest rates stand at rock-bottom levels, US deficit keeps widening, mass SMEs' bankruptcies are lurking, meanwhile, the stock market reached its most expensive level since the Dotcom bubble of 2000, based on its ratio of price to cyclically adjusted profits.

As a matter of fact, long-term deficits can be detrimental for economic growth and stability because they crowd out private borrowing, manipulate interest rates, decrease net exports and lead to either higher taxes, higher inflation or both. US bonds and T-bills attract borrowers because they put their trust in the government's ability to make them whole on their claims. However as debt accrues, trust will slowly erode and refinancing may just become impossible. This is even more believable if we remove payments from the Federal Reserve, due to its large balance sheet, which partially obscure the federal deficit. How long can last a system printing money to refinance its own public debt?

If interest payments on the debt ever become untenable through normal tax-and-borrow revenue streams, the government faces three options. They can cut spending and sell assets to make payments, they can print money to cover the shortfall, or the country can default. Option one and three are No Gos, which leaves one (unorthodox) solution: quantitative easing. The Fed's aggressive expansionary monetary should logically result in high levels of inflation capping the use of this strategy, but once again, text books theories don't materialise. The decrease in velocity seems to cancel the effect of the increase in money supply and thus, inflation remains low. For now, it is unsure what could happen.

Mr Biden's plans are exciting and promising, so as all electoral promises. One variable of the global uncertainty equation was cancelled when Trump had his rattle removed, but it is too early to confirm Biden is not an average Joe. He needs to deliver by the 30/04 milestone (first 100 days), and beyond that, his political agenda will have to address more thorny foreign issues: the Sino-American trade war, relations with NATO and troops in Iraq and Afghanistan, among others.

Sources used in the article: The New York Times, The Economist, The Balance, The National Bureau of Economics Research, Investopedia.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

MT Finance - Mathias Talmant.

Commentaires